Don’t delay

This is the simplest of the two today, you simply cannot afford to delay innovation rollout in your business any further, otherwise you will be left eating dust.

The need to act now, if you haven’t already, is intensified by an important trend we are seeing in our industry.

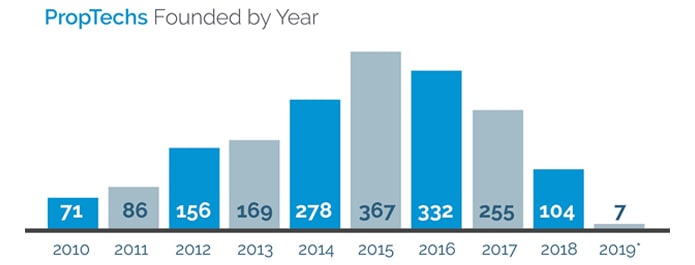

Since 2015, the number of new companies entering the PropTech market has fallen, year-on-year. In 2015, in Europe, 367 new companies appeared. This number has dropped ever since, falling to just 104 in 2018, the lowest since 2011.

This graph shows the full European picture:

At the same time, global PropTech investment has risen while the number of fundraising events has dropped:

- In 2016, there were 1,169 funding events, with a total of $8.8 billion raised, averaging $7.5 million.

- In 2017, we saw 1082 events, a total of $11.5 billion, with an average of $10.7 million.

- In 2018, just 898 events raised $14.9 billion, an average of $16.5 million.

These three observations (fewer new companies, fewer funding events, higher total funding) combine to offer one important insight: PropTech is maturing.

There are less new companies joining the industry because, one, there are fewer vacant niches by the day, and two, the industry is consolidating, less welcoming of new arrivals bringing unimpressive or generic offerings. We saw a similar thing happening in the FinTech market several years back.

PropTech funding’s rise shows steady investor confidence in the industry, and the falling number of events tells us that individual deals are getting bigger.

This trend started in the US, but is now spreading through the UK and Europe, too. Really big, almost obnoxiously big, funding rounds are being closed.

All of this means that anyone who is not firmly onboard the tech train needs to jump on right now. A maturing market means decreased opportunity for real estate firms to put their personal stamp on the tech they’re being offered.

The opportunity for co-creation disappears and those rival firms who jumped on early will suddenly have a competitive advantage that you are going to really struggle to breach.

I expect we’re going to see increased consolidation here in the UK with more and more rival companies coming to realise that they have complementary offerings, that combined, they can offer the customer far more. There will, of course, be others who simply fold under the pressure - a common problem among these companies will likely be founder ego.

I should, at this point, direct you back to my previous articles in this series - all linked above. Part of not delaying is to appreciate the need to embrace, engage, and encourage. They all lead to this point.

So, act now, folks. The market is squeezing and competition is ramping up on both sides of the table. Don’t fall behind, don’t delay.

And, with that, we move seamlessly, some might say poetically, to the next section. For digital innovation is, after all, now a vital part of that age-old practice of enhancing your value proposition…

Do enhance your value proposition

I don’t mean this to sound like a cheap piece of self-help spiel, but we all need to understand our value and our worth. Each real estate firm must understand what their customers are looking for and provide the best solutions.

Further still, they must work to predict what those same customers will be looking for in the future.

When someone moves home, what are they most looking for from their agent? The answer will be both practical and emotional - both are vital and actionable.

I always recommend firms go back and ask their previous customers what, with reflection, they would be looking for next time. What’s important to them? And how could the service be improved?

It might be a case of providing 24-hour support; more opportunity for face-to-face meetings during the sales process; more privacy through unaccompanied viewings; more transparent chain management. You need to know how consumers are measuring the success of their experience.

This all requires substantial research to understand what your past customers think of you now, to understand what your competitors, and the wider industry, is good at now and where it continues to fall short.

Ultimately, you are looking to understand what added value you give now and how you rank against competitors. Then you can start to realise how you can add more value to your business, for both you and your clients. Then you can start to understand future product lines based on what your clients are trying to achieve (not what they want).

I’ll provide one tip, reading Allagent reviews is not sufficient research.

Adding value for sellers

When thinking about sellers (we should always be thinking about sellers because they pay the commission), it’s important to gather as much feedback as you can.

It won’t always be fun reading, but it will give you a checklist of pain points. You will see, in black and white, exactly what is hindering your value proposition.

Now ask yourself, can technology help me solve these pain points? It’s getting easier and easier to then navigate the market to find exactly the right solutions for you.

However, there will also be areas where tech can’t help because it’s more about the personal, human side of your service.

Here, the question becomes, how can we, as a firm, improve the personal interactions with our clients to increase our value proposition and sit head-and-shoulders above the competition?

To touch briefly on the competition - don’t shy away from asking what other firms your past clients have used and how that went for them. What was the difference between us and them?

From my personal experience, although I haven’t been in agency for some time now, is that there isn’t much difference at all. It often comes down to your fees and the individual sales skills of the agent involved.

Looking back at my Foxtons experience, we knew that we were open longer than anyone else. Even Saturdays and Sundays. We provided the service when, back in the early 2000s, no one else (or very few) did; we were proud of this. We were different. We worked hard to drive that difference into every single thing we did. I am still proud of that time.

There are many other ways I can demonstrate this difference of value proposition from back in the day but, ultimately, Foxtons had a different value proposition to everyone else. It served them well.

But, this has all but disappeared now. Everyone copied. Everyone upskilled. Foxtons are, sadly, no longer unique. They need to consider their value proposition and once more differentiate before someone else does it first.

Brands can try to nurture a cross-employee standard of service, but it will always come down to each agent individually. You might find that your value proposition is best enhanced by simply hiring a better, more brazen, more engaging, enthusiastic, and tenacious agent. If so, don’t delay, get it done.

And we can’t ignore the buyers. How can we give them more value? Most buyer leads are now arriving through portals, it’s a simple fact, but I think many forget to realise that, often, buyers eventually become sellers.

Further down the line, if you’ve given a buyer supreme service it will be remembered: it will be spoken about. When the time comes, they will come to you.

So, you’ve got to ask them all of the same questions you’re asking your sellers. What are they looking to achieve? What have they experienced it the past, both good and bad? How could this be improved upon?

It’s vital, in this day and age, to weave technology across your business model, but, I have to stress, it is not everything. I have, for example, looked at the websites of the five top national estate agents and I have absolutely no idea how they differ in product or service. Not one of them made me want to speak to them over and above the rest - not as a buyer, seller, landlord, or tenant.

Clearly, then, market disruption is about more than digital innovation. I would say that having a clear understanding of how you differ from your competitors, and then figuring out how to tell the market so, might just be the best value-adder an agent can have today.

*James Dearsley is a leading PropTech influencer and commentator, and is co-founder of PropTech platform Unissu. You can follow James on Twitter here.

Join the conversation

Be the first to comment (please use the comment box below)

Please login to comment